When people cannot keep up with their bills they may file for bankruptcy as a way to get a fresh financial start. By filing for bankruptcy, you immediately receive what is referred to as an automatic stay, in which creditors cannot seek collection on debts until they have been sorted out. Our Arlington, TX Chapter 13 bankruptcy lawyer can guide you through the process of filing for bankruptcy if that is the best option for you. There are other bankruptcy chapters available so it will be imperative that you file for the one most suited for your situation. We understand that financial stress can take a toll on one’s health and mindset. We are here to provide the solutions and support you need. Do not hesitate to contact Leinart Law Firm today for more information about bankruptcy.

Chapter 13 Bankruptcy

Under Chapter 13 bankruptcy, the debtor pays back some or the entirety of their debts through a 3-5 year repayment plan. In order to qualify, the debtor must have consistent income to meet these payments. Income can include wages, social security, retirement, and disability benefits. With Chapter 13 bankruptcy, a bankruptcy trustee is appointed to oversee the handling of your case, investigate your finances, address creditor claims, ensure the plan is fair, and see that you pay down your debts based on the plan given to you. At the end of the repayment term, the balance of any unsecured debts will be discharged. If you have questions about this, contact our knowledgeable Chapter 13 bankruptcy attorney for a consultation.

Facts To Consider

By filing for Chapter 13 bankruptcy, it allows a debtor who doesn’t qualify to operate under Chapter 7 to reorganize their finances by decreasing monthly payments to creditors. Once the repayment plan duration is complete, any remaining unsecured debt gets discharged. This chapter prevents debt collectors from seeking outstanding debts that are listed in the case. Another fact about Chapter 13 bankruptcy is that it stops repossession of vehicles and other property. It also halts foreclosure on your home and gives you the opportunity to catch up on missed payments. If you are concerned about your finances and are considering bankruptcy, let us meet with you to make sure that is a next step that will benefit you in the long term.

Seek Financial Relief Today

It is important to note that there are things that Chapter 13 cannot do. For instance, past-due child support, IRS debt, property taxes, and most student loans won’t be discharged. It cannot eliminate the right of creditors to secured property, like home mortgages and car loans. After bankruptcy, your home may still get foreclosed and your vehicle repossessed if you fail to make payments. Our Texas Chapter 13 bankruptcy attorney is ready to speak with you about your situation before proceeding further. It is essential that you fully understand what bankruptcy entails and what it can and cannot do for you. If you are ready to start a new financial beginning, then contact Leinart Law Firm as soon as possible.

Repayment Plans In Chapter 13 Bankruptcy

Filing for Chapter 13 bankruptcy offers individuals a chance to reorganize their debts and create a manageable repayment plan and an Arlington chapter 13 bankruptcy lawyer from our firm can be of assistance. Unlike Chapter 7 bankruptcy, which involves liquidating assets to pay off debts, Chapter 13 allows you to keep your property while paying creditors over time. Creating a repayment plan is a crucial step in the Chapter 13 process. Here’s what you need to know about crafting an effective repayment plan.

Understanding The Repayment Plan

A Chapter 13 repayment plan outlines how you will pay back your debts over a three to five-year period. The plan must be approved by the bankruptcy court and is based on your income, expenses, and the type of debts you owe. The goal is to repay creditors as much as possible while allowing you to maintain a reasonable standard of living.

Key Components Of The Repayment Plan

Income Assessment:

1. The first step in creating a repayment plan is to assess your current and projected income. This includes wages, bonuses, rental income, and any other sources of revenue. The court requires proof of stable and sufficient income to ensure you can make the proposed payments throughout the plan’s duration.

Expense Evaluation:

2. Next, you’ll need to detail your monthly living expenses. This includes housing costs, utilities, food, transportation, healthcare, and other necessary expenses. The court will review these expenses to ensure they are reasonable and necessary. Excessive or luxury expenses may be scrutinized or reduced.

Debt Categorization:

3. Your debts will be categorized into three groups: priority, secured, and unsecured.

- Priority Debts: These include taxes, child support, and alimony. These debts must be paid in full over the course of the repayment plan.

- Secured Debts: These are debts backed by collateral, such as mortgages and car loans. Your plan must address how these debts will be handled, whether through continued payments or catching up on arrears.

- Unsecured Debts: These include credit card debt, medical bills, and personal loans. While these debts do not have to be paid in full, you must demonstrate that you are paying as much as possible based on your disposable income.

Calculating Disposable Income:

Disposable income is the amount left after subtracting your monthly living expenses from your monthly income. This amount will be used to pay your unsecured creditors. The more disposable income you have, the more you will pay towards these debts.

Setting Payment Terms:

Your repayment plan will specify the amount and frequency of payments to the bankruptcy trustee, who will distribute funds to your creditors. Payments are typically made monthly. Consistency is key, as missed payments can result in the dismissal of your bankruptcy case.

Adjusting For Changes:

Life circumstances can change, and your repayment plan can be modified to reflect significant changes in income or expenses. If you experience a job loss, medical emergency, or other financial hardship, you can petition the court to adjust your plan accordingly.

Legal Guidance From Our Firm

Creating a repayment plan in Chapter 13 bankruptcy requires careful assessment of your financial situation and a commitment to following through with the payments. By working diligently to craft a feasible plan and adhering to its terms, you can navigate the bankruptcy process effectively and work towards a more secure financial future. If you’re considering Chapter 13 bankruptcy, taking the time to understand and prepare for the repayment plan process is a crucial step in achieving debt relief and long-term financial health. Reach out today to speak with a chapter 13 bankruptcy lawyer Arlington TX trusts from Leinart Law Firm.

The Impact Of Bankruptcy On Your Future Financial Opportunities

Filing for bankruptcy is a significant decision, one that many people find themselves contemplating during times of financial distress. At Leinart Law Firm, we understand the weight of this decision and its potential impact on your future financial opportunities. Here, we explore how bankruptcy can influence various aspects of your financial life.

- Credit Score and Credit History: One of the most immediate impacts of bankruptcy is on your credit score. Filing for bankruptcy can cause a substantial drop in your score, typically between 130 to 200 points, depending on your initial score. This negative mark can stay on your credit report for up to 10 years for Chapter 7 and up to 7 years for Chapter 13. However, with diligent effort, it’s possible to rebuild your credit over time. Many people in Arlington find that working with an Arlington chapter 13 bankruptcy lawyer can provide guidance on how to start this rebuilding process effectively.

- Access to Credit: Post-bankruptcy, obtaining credit can be challenging. Lenders may view you as a high-risk borrower, leading to higher interest rates and stricter terms. Initially, you might only qualify for secured credit cards or loans with higher interest rates. Over time, as you demonstrate responsible financial behavior, your access to credit will improve. It’s important to stay consistent and avoid the pitfalls that led to bankruptcy in the first place.

- Loan Eligibility: Securing loans for significant purchases like a home or car can be more difficult after bankruptcy. Mortgage lenders, in particular, may require a waiting period before considering your application—usually two to four years after discharge. Auto loans might be easier to obtain but expect higher interest rates initially. Consulting with an Arlington bankruptcy lawyer can help you understand the specific timelines and requirements for loan eligibility post-bankruptcy.

- Employment Opportunities: While bankruptcy does not directly affect your current employment, it can influence future job prospects. Some employers conduct credit checks as part of their hiring process, especially for positions that involve financial responsibility or access to sensitive information. Although it’s less common, some employers might view a bankruptcy filing negatively. Being transparent about your financial recovery and demonstrating your commitment to better financial practices can mitigate these concerns.

- Renting a Home: Finding a rental home can be more complicated after bankruptcy. Landlords often conduct credit checks and may view a bankruptcy as a red flag. However, many landlords in Arlington are willing to consider your current financial situation and your explanations for the bankruptcy. Providing proof of income, references, and a solid rental history can improve your chances of securing a rental property.

- Insurance Rates: Insurance companies sometimes use credit scores to determine premiums. A bankruptcy filing can lead to higher premiums for auto, home, and even life insurance. Over time, as you improve your credit score, you can shop around for better rates or negotiate with your current provider for lower premiums.

Assistance From Our Law Firm

Filing for bankruptcy is not the end of your financial journey but rather a new beginning. At Leinart Law Firm, we are committed to helping you understand the impact of bankruptcy on your future financial opportunities and guiding you through the process. If you’re considering bankruptcy, reach out to us for a consultation with a chapter 13 bankruptcy lawyer Arlington TX trusts. Let us help you take the first step toward financial recovery and a brighter future. Contact us today to learn more about how we can assist you.

Arlington Chapter 13 Bankruptcy Infographic

Arlington Chapter 13 Bankruptcy Statistics

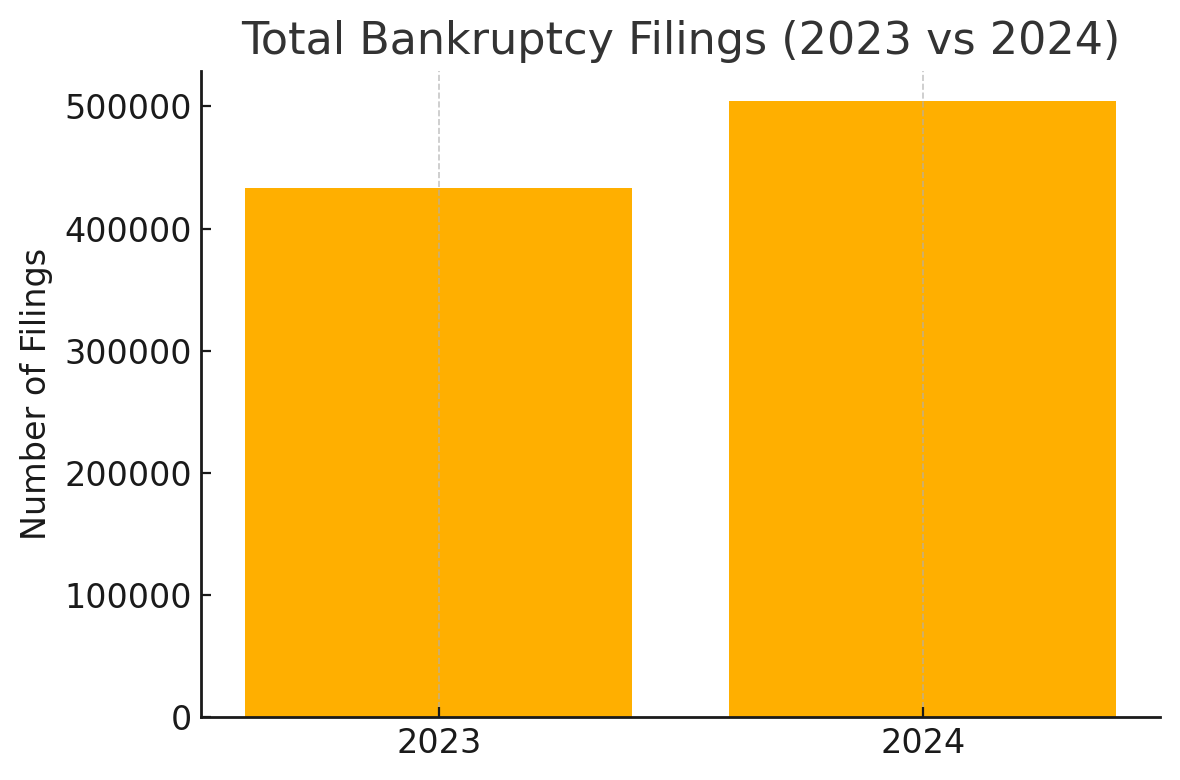

Bankruptcy filings in the United States have experienced notable fluctuations in recent years, reflecting the nation’s economic dynamics. In the 12-month period ending September 30, 2024, there were 504,112 bankruptcy cases filed, a 16.2% increase from the 433,658 filings in the previous year.

This rise was primarily driven by a 33.5% surge in business bankruptcy filings, which escalated from 17,051 to 22,762 during the same timeframe. Conversely, non-business (personal) bankruptcy filings saw a 15.5% rise, reaching 481,350 compared to 416,607 in the prior year. These statistics underscore the evolving financial challenges faced by both individuals and businesses in the current economic landscape.

Arlington Chapter 13 Bankruptcy FAQs

Filing for Chapter 13 bankruptcy can be an effective way to manage and repay your debts while keeping your assets. Understanding which debts are included in the repayment plan is crucial for planning and ensuring that your financial obligations are met. At Leinart Law Firm, we are committed to helping individuals in Arlington, TX, navigate the complexities of Chapter 13 bankruptcy. Below, we answer some frequently asked questions about the types of debts included in a Chapter 13 repayment plan.

Which Debts Are Prioritized In A Chapter 13 Repayment Plan?

In a Chapter 13 repayment plan, debts are categorized and prioritized to ensure that certain obligations are paid before others. Priority debts are the first to be addressed. These include debts such as child support, alimony, and certain tax obligations. These debts must be paid in full through the repayment plan. Ensuring these debts are prioritized helps prevent further legal complications and supports compliance with court mandates.

Are Mortgage Arrears Included In The Repayment Plan?

Yes, if you have fallen behind on your mortgage payments, the arrears can be included in your Chapter 13 repayment plan. This inclusion allows you to catch up on missed payments over the life of the plan while keeping your home. Regular mortgage payments must continue to be made outside the plan. Including mortgage arrears in the plan can help avoid foreclosure and provide a structured approach to managing overdue payments.

Can Credit Card Debts Be Part Of The Repayment Plan?

Credit card debts, which are considered unsecured debts, can be included in the repayment plan. Unsecured debts do not have collateral backing them and include medical bills, personal loans, and credit card balances. While these debts are typically lower in priority, a portion of the disposable income will be allocated towards repaying them over the three to five years of the plan. Including unsecured debts like credit cards helps create a comprehensive approach to debt management. An Arlington chapter 13 bankruptcy lawyer can assist you with these types of debts.

What Happens To Secured Debts In Chapter 13 Bankruptcy?

Secured debts, such as car loans or home equity loans, are also included in the Chapter 13 repayment plan. These debts are backed by collateral, meaning the lender can repossess the asset if the debt is not paid. The repayment plan will address these debts, allowing you to pay off the arrears and keep the assets. It’s important to continue making regular payments on these debts outside the plan to prevent repossession.

Are Student Loans Included In The Repayment Plan?

Student loans are included in the Chapter 13 repayment plan as unsecured debts. However, they are treated differently than other unsecured debts. While you will make payments toward student loans during the plan, any remaining balance at the end of the plan period will not be discharged. This means you will still be responsible for any remaining student loan debt after completing the Chapter 13 plan. Addressing student loans within the plan provides a structured repayment approach, although it does not eliminate the obligation entirely.

If you are considering Chapter 13 bankruptcy and need guidance on how to proceed, consulting with an experienced Arlington, TX chapter 13 bankruptcy lawyer is crucial. At Leinart Law Firm, we are dedicated to helping you achieve financial stability. Contact us today for a consultation and take the first step towards a brighter financial future.

Arlington Chapter 13 Bankruptcy Glossary

At Leinart Law Firm, we help clients understand what to expect when working with an Arlington, TX chapter 13 bankruptcy lawyer. The legal process of debt relief can involve several important terms and procedures that impact how repayment plans are structured and approved. Below, we’ve explained several key terms that often come up in Chapter 13 cases, so you can move forward with clarity and confidence.

Repayment Plan

A repayment plan is a formal proposal submitted to the bankruptcy court that outlines how a debtor will repay creditors over a period of three to five years. This plan includes details about income, expenses, secured debts, and unsecured debts. The court must approve this plan before it becomes binding. Monthly payments are typically made to a bankruptcy trustee, who then distributes the funds to creditors. This plan is central to any Chapter 13 filing and must show that the debtor will use their disposable income to meet financial obligations.

Bankruptcy Trustee

A bankruptcy trustee is a court-appointed official responsible for administering the repayment plan in a Chapter 13 case. This individual reviews the proposed plan, collects payments from the debtor, and distributes the funds to creditors. The trustee also monitors compliance with the plan terms and may raise objections if the plan does not meet legal standards. In addition to payment oversight, the trustee may conduct a meeting of creditors, known as a 341 meeting, to allow creditors to ask questions about the case.

Automatic Stay

An automatic stay is a court order that takes effect immediately when a bankruptcy case is filed. This stay halts most collection actions, including wage garnishments, lawsuits, repossessions, and foreclosure proceedings. It provides relief to debtors by temporarily stopping creditor actions and giving time to work through the Chapter 13 process. While the stay can be lifted under certain circumstances, it typically remains in place throughout the repayment period unless the court decides otherwise.

Priority Debt

Priority debt refers to specific obligations that must be paid in full through a Chapter 13 plan before other unsecured debts receive payment. Examples include recent income taxes, child support, and alimony. These debts cannot be discharged through bankruptcy and are treated differently from general unsecured debts such as credit card balances or medical bills. The repayment plan must clearly address how priority debts will be paid to gain court approval.

Secured Claim

A secured claim is a debt backed by collateral, such as a home mortgage or auto loan. In a Chapter 13 case, the debtor may continue paying the secured debt through the plan or work out arrangements to modify the terms. In some instances, the plan may allow for a reduction of the loan balance if the collateral is worth less than the debt owed. This process, sometimes called a “cramdown,” can help debtors keep essential property while making payments more manageable.

Contact Our Arlington Chapter 13 Bankruptcy Lawyer Today

If you’re considering filing for Chapter 13, working with an Arlington, TX chapter 13 bankruptcy lawyer can help you create a clear path toward financial stability. Contact Leinart Law Firm today to schedule a confidential consultation and learn how we can help you move forward with a structured plan for your future.